Questions about the Manhattan or Brooklyn real estate markets or the value of your property? Contact Daniel

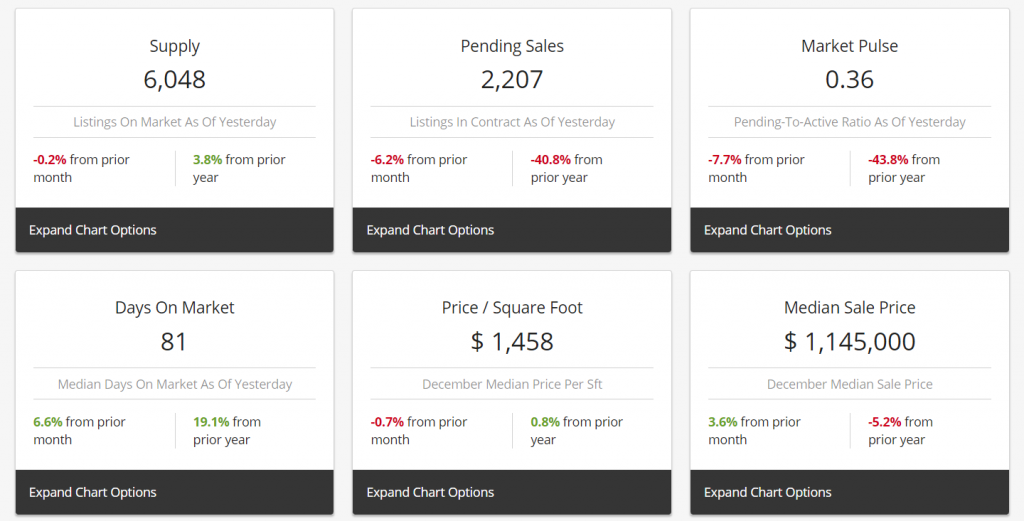

Market Snapshot

To read all the detailed data, download the full report here

Happy New Year from QHT! We hope your 2023 has kicked off to a great start. Here at QHT, as we started the year, we were doing a lot of business-planning and preparation for the coming 2023 housing market in anticipation of the shifts and changes we expect to see throughout the year. There is understandably a lot of caution and concern out there among consumers and homeowners, so now, more than ever, it’s important for us to keep our fingers on the pulse of the market in order to guide our clients and readers properly.

With that idea in mind, we present to you here a market snapshot for the last quarter of 2022, as well as some insights on what we are seeing as we kick off 2023. If you’d really like to dig into the numbers and the data, we’ve included a full downloadable report for you.

As you may have noticed, heading into 2023 the market was pretty slow in terms of sales activity. Last year’s big headline and market driver was the high inflation rate, and the resulting rapid rise in mortgage rates. Although interest rates still remain below historic averages (the 30 year average mortgage interest rate is around 8%), the pace of interest increase led to whiplash and sticker shock for many buyers. These factors then led to additional fears of a recession and contributed to a plummeting stock market and several other consequences that influenced the real estate market and will likely continue to some degree into 2023.

The good news is that inflation seems to have peaked and is now normalizing, and mortgage rates appear to have peaked back in late October. Since then, they have come down significantly. As inflation continues to settle down – which is what is being predicted by many pundits – we can expect interest rates to level off or reduce further. The recession talk has been hit or miss, and there isn’t widespread agreement on whether we are in one, or will see one in 2023. In fact, there isn’t even agreement on how to define a recession in our current environment! However, if we do enter a recession, then it’s possible we will see interest rates drop further as the Fed adjusts to counteract that.

The last quarter of the year was slow in terms of activity and demand, but it was also slow in terms of new listings hitting the market. We typically see a slowdown during the holidays anyway, but all of the economic factors we mentioned made the slowdown even more pronounced. Mortgage rates were rising all year, at a pace we’ve never seen, and as they rose demand was definitely declining in real time. The slowdown in the market has, so far, had a modest impact on Manhattan sales prices, and many other metrics are stable, indicating we may be settling into a new normal. Certainly, Manhattan experienced more negative price impact than either Queens or Brooklyn, with about a 6% drop in Median sale price across 2022 compared to 2021. However, inventory is low and continues to fall, which prevents prices from dropping too much given the demand that is there.

An interesting fact was that the price per square foot actually INCREASED by 2.6% in 2022. One possible interpretation is that, while the increased interest rates obliterated whatever affordability buyers found in the 2021 Manhattan market as a result of the 2020 pandemic exodus, there was still demand to buy homes and buyers were simply forced to buy smaller apartments with the money they had in order to afford the monthly payments.

As we head into 2023, the market is feeling stronger, mainly because for the last 8 weeks of 2022, mortgage rates were trending downward going from around 7.5% to around 6.5%, and the trend has continued into January. Some pundits feel mortgage rates may settle in the 5.5-6.0% range in 2023. As you can imagine, that has led to an uptick in buyer activity. According to a report from CNBC, mortgage applications actually shot up 28% in the first week of January, a sign that there is still pent up demand out there and buyers may just be waiting for a reason to jump back in. Couple this with continuously low inventory levels and you get a market that in many respects feels like a buyer’s market, but in other ways is behaving like a pretty balanced market. This is borne out by the fact that month’s supply in Manhattan is hovering at 4.8 months, which is right in the “balanced market” range of 5-7 months of inventory.

All in all, the Manhattan real estate market is in for another year of uncertainty. There’s plenty of speculation and many predictions out there, but we aren’t confident enough to make one of our own given all the unknowns. One thing we are fairly confident of is that prices in Manhattan should continue a modest decline, but unless inventory grows significantly, it’s hard to imagine a scenario where prices come down dramatically. The other thing we do know is that in order for sellers to sell and sell quickly (which is always advantageous), they will need to be modest on their pricing throughout 2023 and be sensitive to the buyers’ needs to find a good value. Despite the balanced inventory, buyers currently hold the upper hand when it comes to leverage and negotiations. How this plays out in terms of property prices and ease of sale in specific sectors of the Manhattan market will be interesting to watch as 2023 moves into the spring selling season. We’ll see how it all plays out and keep you posted.

Questions about the Manhattan or Brooklyn real estate markets or the value of your property? Contact Daniel

To read all the detailed data, download the full report here